Whether you’re a student learning accounting for the first time, a small business owner trying to make sence of your books, or just someone who wants to understand how financial records actually work — this guide will walk you through debit vs credit rules in the simplest way possible. We’ll go over the golden rules of accounting, practical journal entry examples, T-accounts, and the most commmon mistakes beginners make. By the time you finish reading, debits and credits will feel a lot less scary.

What Are Debits and Credits — Really?

In everyday life, people use “debit” to mean money leaving their account and “credit” to mean money arriving. But in accounting, these words have a completly different meaning. Debits and credits are simply the two sides of every financial transaction recorded under the double-entry bookkeeping system.

Every transaction affects at least two accounts — one gets debited and the other gets credited. This is the entire foundation of double-entry accounting, a system that has been used by businesses for over 500 years. The goal is simple: keep the accounting equation balanced at all times — Assets = Liabilities + Equity.

📤 Debit (Dr)

Always recorded on the left side of a T-account.

- Increases Assets

- Increases Expenses

- Decreases Liabilities

- Decreases Revenue

- Decreases Equity

📥 Credit (Cr)

Always recorded on the right side of a T-account.

- Increases Liabilities

- Increases Revenue

- Increases Equity

- Decreases Assets

- Decreases Expenses

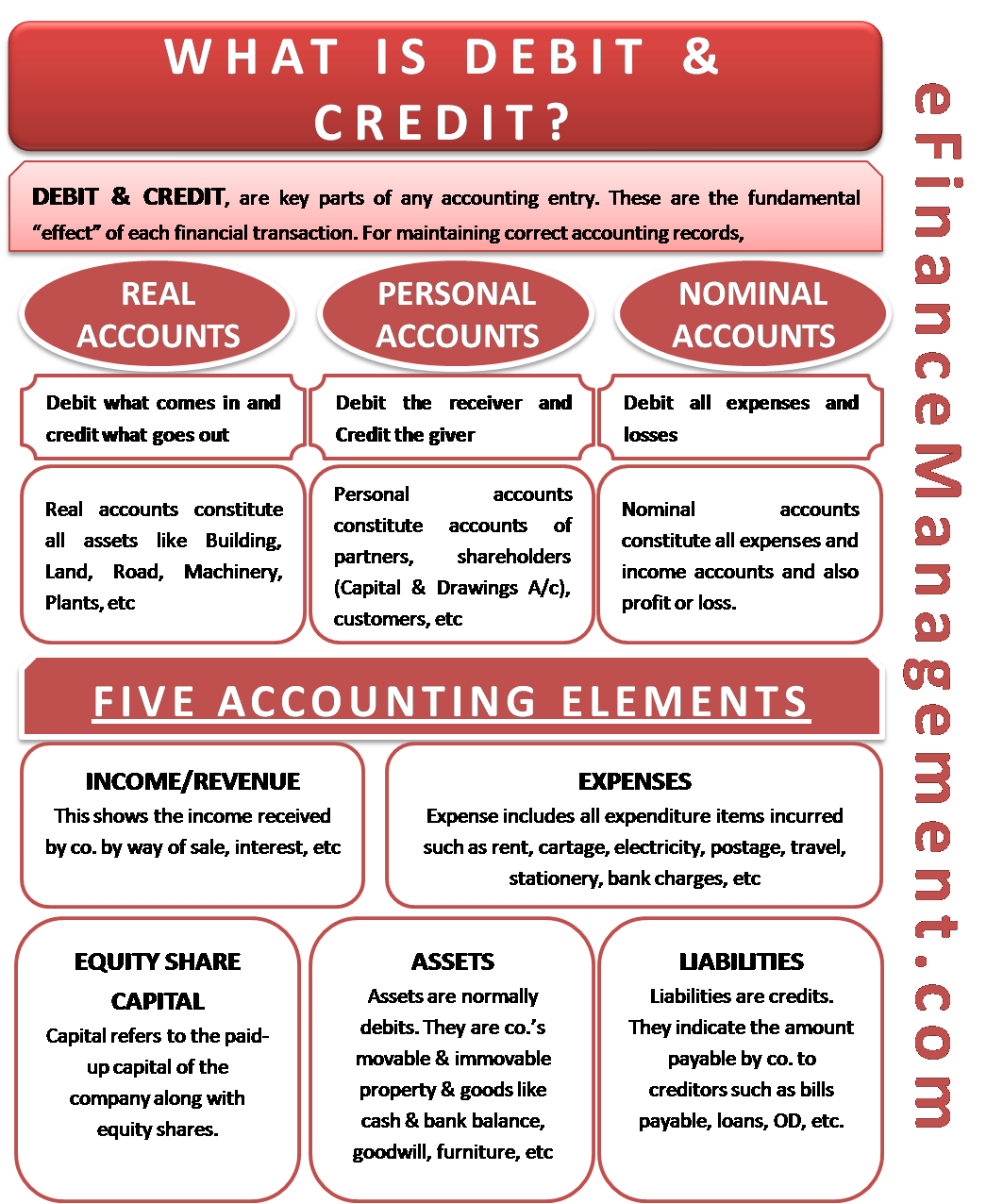

The Three Golden Rules of Accounting

To make debit and credit decisions easier, accountants use the famous “Golden Rules of Accounting.” These rules are tied to the three types of accounts — Real, Personal, and Nominal — and they tell you exactly when to debit and when to credit in any situation. If you want to get good at bookkeeping, these are the rules you should memorise first.

| Account Type | Debit Rule | Credit Rule | Examples |

|---|---|---|---|

| Real Account | What comes in | What goes out | Cash, Machinery, Land |

| Personal Account | The receiver | The giver | Debtors, Creditors, Bank |

| Nominal Account | Expenses & losses | Incomes & gains | Rent, Salary, Sales |

Once you know wich rule applies to each account type, you’ll stop second-guessing yourself when recording transactions. These three rules cover every possible financial situation a business can face.

Understanding the T-Account

A T-account is the most visual and practical way to understand how debits and credits actually work. It looks like the letter “T” — the left side shows all debits and the right side shows all credits. Every account in the ledger can be represented as a T-account, which helps you quickly see how transactions are effecting the balance.

Example: Cash Account (Real Account)

Closing Balance (Debit): $15,500 − $4,500 = $11,000

The cash account has more debits than credits, which means the business holds a positive cash balance of $11,000. This is how every account in the general ledger operates — transactions accumulate on both sides, and the diffrence between them gives you the closing balance.

Practical Journal Entry Examples

Let’s look at some real-world transactions so you can see these debit and credit rules in pratice. Understanding how entries are recorded makes the whole concept click much faster than just reading theory.

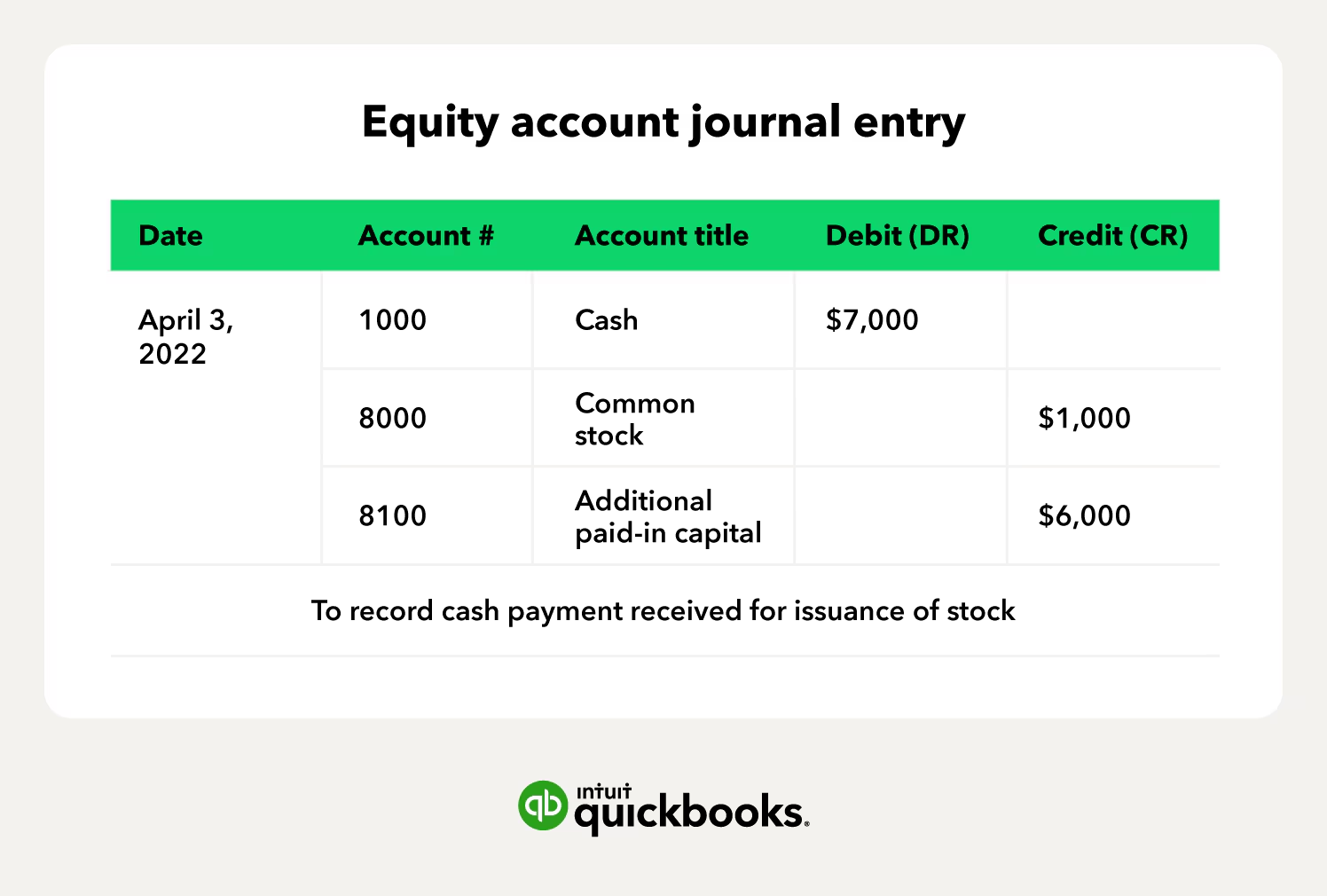

Example 1 — Starting a Business

Transaction: Ahmed starts a business by investing $20,000 cash.

✅ Debit: Cash Account $20,000 — cash is coming into the business (Real Account)

✅ Credit: Capital Account $20,000 — Ahmed is the giver (Personal Account)

Example 2 — Purchased Goods on Credit

Transaction: Bought goods worth $5,000 from a supplier named Bilal on credit.

✅ Debit: Purchases Account $5,000 — it’s an expense (Nominal Account)

✅ Credit: Bilal’s Account $5,000 — Bilal is the giver (Personal Account)

Example 3 — Paid Office Rent

Transaction: Paid $1,500 cash as office rent for the month.

✅ Debit: Rent Expense $1,500 — it’s an expense or loss (Nominal Account)

✅ Credit: Cash Account $1,500 — cash is going out (Real Account)

Example 4 — Sold Goods for Cash

Transaction: Sold merchandise worth $8,000 for cash.

✅ Debit: Cash Account $8,000 — cash comes in (Real Account)

✅ Credit: Sales Account $8,000 — it’s income or gain (Nominal Account)

Debit and Credit in Accounting Software

You might be thinking — “I use QuickBooks or Wave, so why do I even need to know this stuff?” That’s a fair question. But here’s the truth: accounting software makes mistakes, and if you don’t understand the rules it’s following, you won’t catch those mistakes until it’s too late. Every time you record an invoice, log a payment, or categorize an expense, the software is applying these exact debit and credit rules in the background.

Some software replaces these terms with “increase” and “decrease” or positive and negative numbers — but the underlying logic is completly identical. A business owner who truly understands debit vs credit will always have better controll over their financial reports than someone who just trusts whatever numbers appear on screen.

Common Mistakes Beginners Make

Mistake 1 — Thinking Debit Always Means a Decrease: A lot of beginers assume that debiting an account reduces it. That’s not always true. Debiting an asset account actually increases it. Only liability and equity accounts go down when debited. This mix-up causes a lot of unnecesary confusion early on.

Mistake 2 — Getting Confused by Bank Statements: When your bank says your account has been “credited,” they mean money came in from their point of view. But in your own books, that same transaction is recorded as a debit to your Cash Account. The perspective is reversed, and this trips up almost every beginner at some point.

Mistake 3 — Recording Only One Side: Double-entry accounting requires every transaction to affect atleast two accounts. If you only record one side, your books won’t balance and your financal statements will be inaccurate. Always make sure the total debits equal the total credits for every entry.

Quick Reference — Debit vs Credit at a Glance

Liabilities ↑ = Credit

Expenses ↑ = Debit

Revenue ↑ = Credit

Equity ↑ = Credit

Cash In = Debit

Cash Out = Credit

Wrapping Up

Debit vs credit is one of those things that sounds complicated at first but starts making perfect sence once you see the logic behind it. The trick is to stop thinking about these words the way your bank uses them and start thinking of them simply as the left side and right side of every transaction.

Learn the three golden rules, practice with real examples, sketch out T-accounts when something confuses you, and always double-check that your entries are balanced. Whether you’re doing your books by hand or using accounting software, these foundational rules will guide every financial decision you make.

Accounting isn’t about memorizing rules — it’s about understanding the story that every number is trying to tell.