1. Assets — What the Business Owns

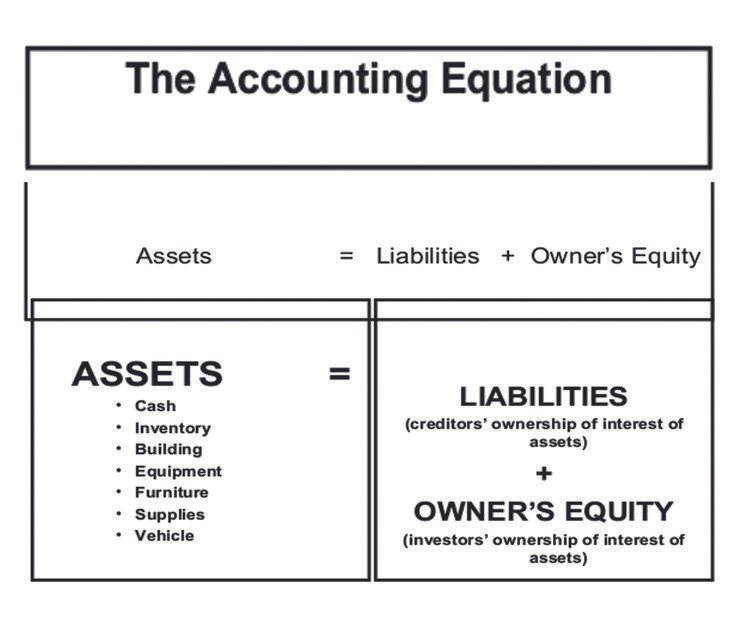

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

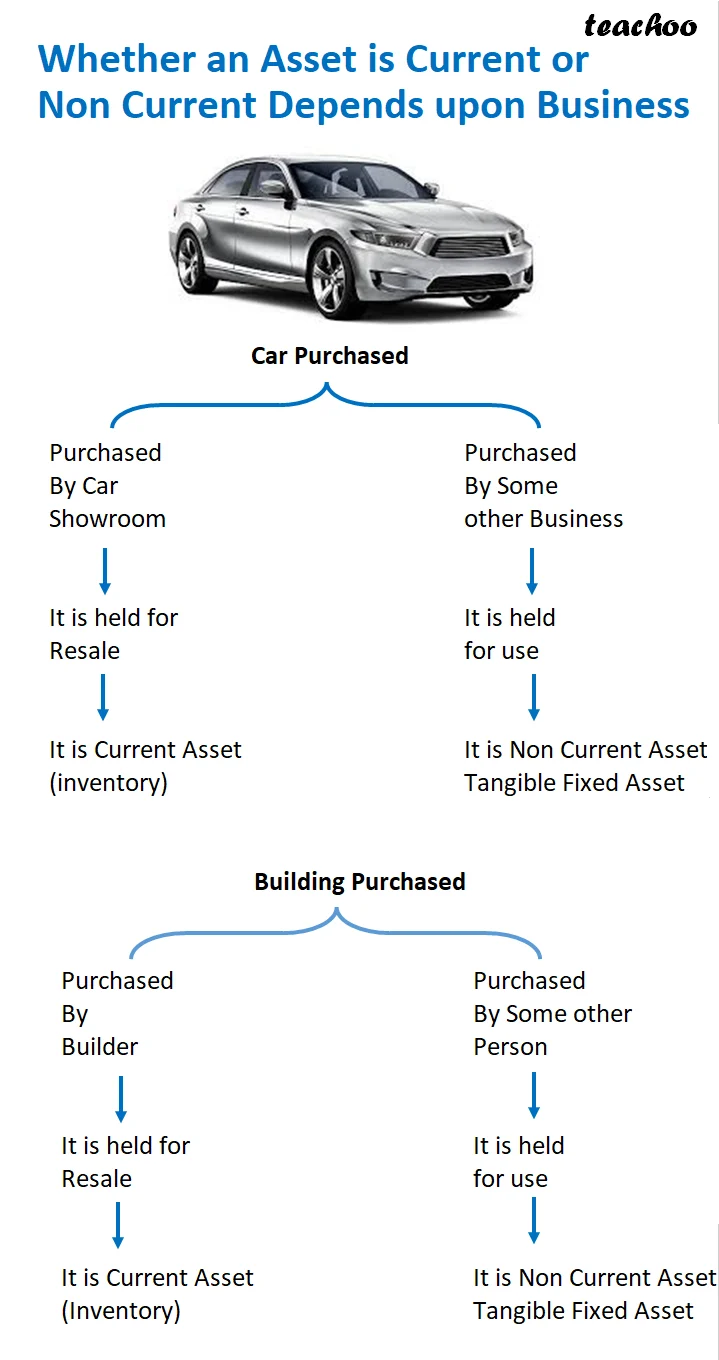

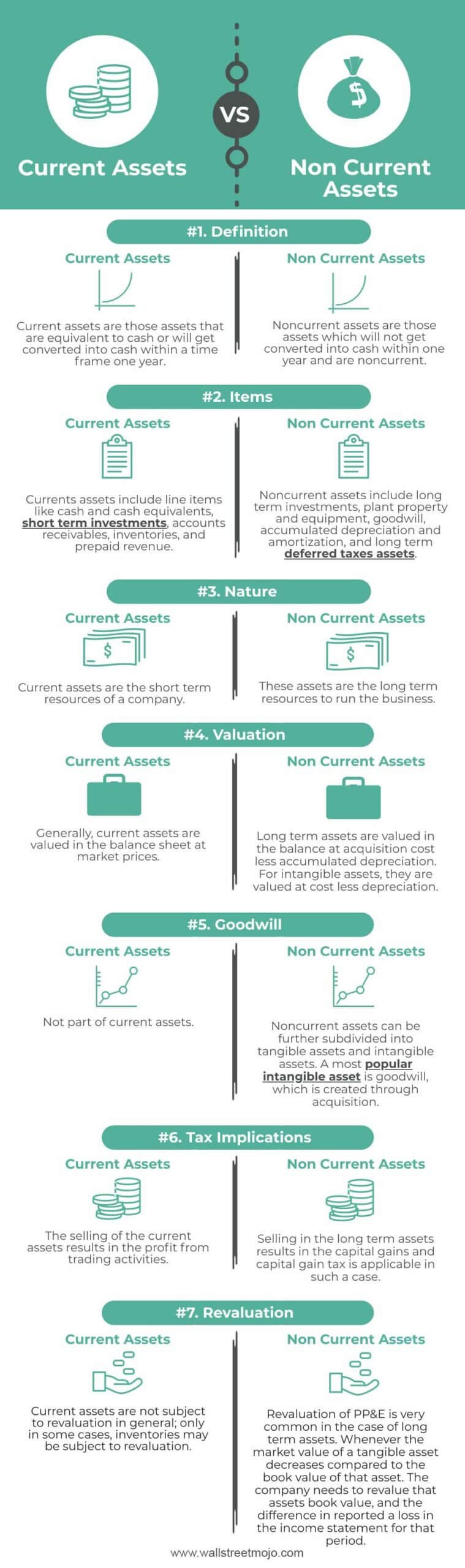

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?

This is one of the most common questions beginers ask. The answer lies in the double-entry bookkeeping system. Every single financial transaction affects at least two accounts — one is debited and another is credited — and both sides are always equal. This means no matter how many transactions a business records, the accounting equation will always remain in balance.

Think of it like a seesaw — whenever something is added to one side, something equal is either added to the other side or removed from the same side. The balance is always maintained automaticaly by the nature of double-entry accounting itself.

The Accounting Equation in Action — Real Examples

Let’s walk through some practical transactions to see how the accounting equation stays balanced in every situation. This is where theory meets reality.

How Transactions Affect the Accounting Equation

Example 1 — Owner Invests Cash

Transaction: Sarah starts a business by investing $50,000 of her own cash.

✅ Assets increase: Cash +$50,000

✅ Equity increases: Capital +$50,000

$50,000 = $0 + $50,000 ✔ Balanced

Example 2 — Bought Equipment on Loan

Transaction: Business takes a bank loan of $20,000 to purchase machinery.

✅ Assets increase: Machinery +$20,000

✅ Liabilities increase: Bank Loan +$20,000

$70,000 = $20,000 + $50,000 ✔ Balanced

Example 3 — Earned Revenue

Transaction: Business earns $8,000 by providing services to a client.

✅ Assets increase: Cash +$8,000

✅ Equity increases: Retained Earnings +$8,000

$78,000 = $20,000 + $58,000 ✔ Balanced

Example 4 — Paid an Expense

Transaction: Business pays $2,000 cash as office rent.

✅ Assets decrease: Cash -$2,000

✅ Equity decreases: Retained Earnings -$2,000

$76,000 = $20,000 + $56,000 ✔ Balanced

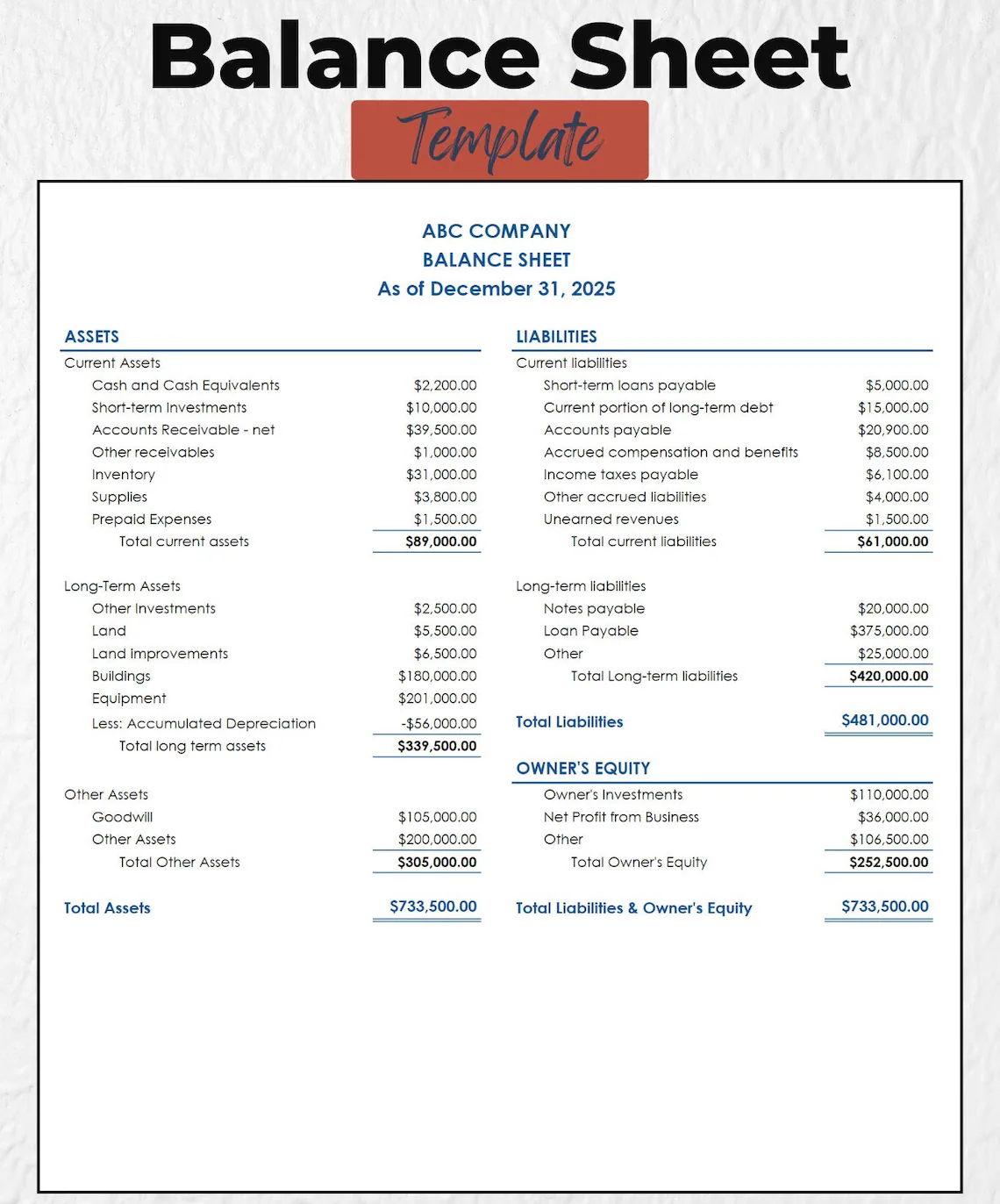

The Accounting Equation and the Balance Sheet

The balance sheet is basically the accounting equation presented in a formal document. When a business prepares its balance sheet at the end of an accounting period, it is simply organizing all its assets on one side and all its liabilities and equity on the other side — and proving that both sides are equal.

This is why the balance sheet is sometimes called the “Statement of Financial Position” — because it shows the exact financial position of a business at a specific point in time. If your balance sheet balances, it means all your transactions have been recorded corectly. If it doesn’t balance, somthing went wrong and you need to find the error.

Sample Balance Sheet — Assets = Liabilities + Equity

Extended Accounting Equation

As you go deeper into accounting, you’ll come across a more expanded version of the basic equation. Since equity is made up of several components, the equation can be written as:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

Expanded form showing all equity components

This expanded version is extremly useful for understanding how day-to-day business activities like earning revenue, paying expenses, and making withdrawals all affect the overall financial position. Each component plays its own role in either increasing or decreasing the owner’s equity.

Extended Accounting Equation with Revenue, Expenses & Drawings

| Component | Effect on Equity | Example |

|---|---|---|

| Capital Invested | Increases ↑ | Owner puts money in |

| Revenue Earned | Increases ↑ | Sales, service income |

| Expenses Paid | Decreases ↓ | Rent, salaries, utilities |

| Drawings | Decreases ↓ | Owner withdraws cash |

Common Mistakes Beginners Make

Mistake 1 — Thinking Assets Must Always Be Larger: Many beginers assume that a business with more assets is always in better shape. But if those assets are mostly financed through debt (liabilities), the business could actually be in a risky financial position. Always look at the equity portion too.

Mistake 2 — Forgetting That Expenses Reduce Equity: A lot of students forget that when a business pays an expense, it doesn’t just reduce assets — it also reduces equity through retained earnings. Both sides must reflect this change for the equation to stay balanced.

Mistake 3 — Confusing Drawings with Expenses: Owner’s drawings are not business expenses — they are withdrawals from equity. Many small business owners mix these up and end up with inacurate financial statements. Always record drawings as a reduction in equity, not as an operating expense.

Quick Memory Trick 💡

Remember the accounting equation with this simple phrase:

“What you OWN = What you OWE + What’s YOURS”

Liabilities = Owe

Equity = Yours

Always Balanced

Final Thoughts

The accounting equation — Assets = Liabilities + Equity — is not just a formula you memorize for an exam and then forget. It is the living, breathing foundation of every financial transaction your business ever records. Every invoice, every payment, every loan, every sale — all of it flows through this single equation.

Once you really understand what assets, liabilities, and equity mean — and how they interact with each other — reading a balance sheet stops feeling intimidating and starts feeling like reading a story about a business. A story about where the money came from, where it went, and what’s left at the end of the day.

Master this equation, and you’ve mastered the language of accounting.

To truly understand the accounting equation, you need to understand what each of the three components actually means in the real world. Let’s go through each one carefully.

1. Assets — What the Business Owns

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?

This is one of the most common questions beginers ask. The answer lies in the double-entry bookkeeping system. Every single financial transaction affects at least two accounts — one is debited and another is credited — and both sides are always equal. This means no matter how many transactions a business records, the accounting equation will always remain in balance.

Think of it like a seesaw — whenever something is added to one side, something equal is either added to the other side or removed from the same side. The balance is always maintained automaticaly by the nature of double-entry accounting itself.

The Accounting Equation in Action — Real Examples

Let’s walk through some practical transactions to see how the accounting equation stays balanced in every situation. This is where theory meets reality.

How Transactions Affect the Accounting Equation

Example 1 — Owner Invests Cash

Transaction: Sarah starts a business by investing $50,000 of her own cash.

✅ Assets increase: Cash +$50,000

✅ Equity increases: Capital +$50,000

$50,000 = $0 + $50,000 ✔ Balanced

Example 2 — Bought Equipment on Loan

Transaction: Business takes a bank loan of $20,000 to purchase machinery.

✅ Assets increase: Machinery +$20,000

✅ Liabilities increase: Bank Loan +$20,000

$70,000 = $20,000 + $50,000 ✔ Balanced

Example 3 — Earned Revenue

Transaction: Business earns $8,000 by providing services to a client.

✅ Assets increase: Cash +$8,000

✅ Equity increases: Retained Earnings +$8,000

$78,000 = $20,000 + $58,000 ✔ Balanced

Example 4 — Paid an Expense

Transaction: Business pays $2,000 cash as office rent.

✅ Assets decrease: Cash -$2,000

✅ Equity decreases: Retained Earnings -$2,000

$76,000 = $20,000 + $56,000 ✔ Balanced

The Accounting Equation and the Balance Sheet

The balance sheet is basically the accounting equation presented in a formal document. When a business prepares its balance sheet at the end of an accounting period, it is simply organizing all its assets on one side and all its liabilities and equity on the other side — and proving that both sides are equal.

This is why the balance sheet is sometimes called the “Statement of Financial Position” — because it shows the exact financial position of a business at a specific point in time. If your balance sheet balances, it means all your transactions have been recorded corectly. If it doesn’t balance, somthing went wrong and you need to find the error.

Sample Balance Sheet — Assets = Liabilities + Equity

Extended Accounting Equation

As you go deeper into accounting, you’ll come across a more expanded version of the basic equation. Since equity is made up of several components, the equation can be written as:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

Expanded form showing all equity components

This expanded version is extremly useful for understanding how day-to-day business activities like earning revenue, paying expenses, and making withdrawals all affect the overall financial position. Each component plays its own role in either increasing or decreasing the owner’s equity.

Extended Accounting Equation with Revenue, Expenses & Drawings

| Component | Effect on Equity | Example |

|---|---|---|

| Capital Invested | Increases ↑ | Owner puts money in |

| Revenue Earned | Increases ↑ | Sales, service income |

| Expenses Paid | Decreases ↓ | Rent, salaries, utilities |

| Drawings | Decreases ↓ | Owner withdraws cash |

Common Mistakes Beginners Make

Mistake 1 — Thinking Assets Must Always Be Larger: Many beginers assume that a business with more assets is always in better shape. But if those assets are mostly financed through debt (liabilities), the business could actually be in a risky financial position. Always look at the equity portion too.

Mistake 2 — Forgetting That Expenses Reduce Equity: A lot of students forget that when a business pays an expense, it doesn’t just reduce assets — it also reduces equity through retained earnings. Both sides must reflect this change for the equation to stay balanced.

Mistake 3 — Confusing Drawings with Expenses: Owner’s drawings are not business expenses — they are withdrawals from equity. Many small business owners mix these up and end up with inacurate financial statements. Always record drawings as a reduction in equity, not as an operating expense.

Quick Memory Trick 💡

Remember the accounting equation with this simple phrase:

“What you OWN = What you OWE + What’s YOURS”

Liabilities = Owe

Equity = Yours

Always Balanced

Final Thoughts

The accounting equation — Assets = Liabilities + Equity — is not just a formula you memorize for an exam and then forget. It is the living, breathing foundation of every financial transaction your business ever records. Every invoice, every payment, every loan, every sale — all of it flows through this single equation.

Once you really understand what assets, liabilities, and equity mean — and how they interact with each other — reading a balance sheet stops feeling intimidating and starts feeling like reading a story about a business. A story about where the money came from, where it went, and what’s left at the end of the day.

Master this equation, and you’ve mastered the language of accounting.

If there’s one formula that every accountant, student, or business owner absolutly must know — it’s the accounting equation. Three simple words: Assets, Liabilities, and Equity. But behind those three words lies the entire logic of how modern accounting works.

Whether you’re just starting to learn accounting, running a small business, or trying to make sence of a balance sheet for the first time — understanding the accounting equation is the single best place to start. In this article, we’ll break down what the accounting equation actually means, why it always stays balanced, how each component works, and how it connects to real business transactions. By the end, you’ll see why this simple formula is the backbone of all financial reporting.

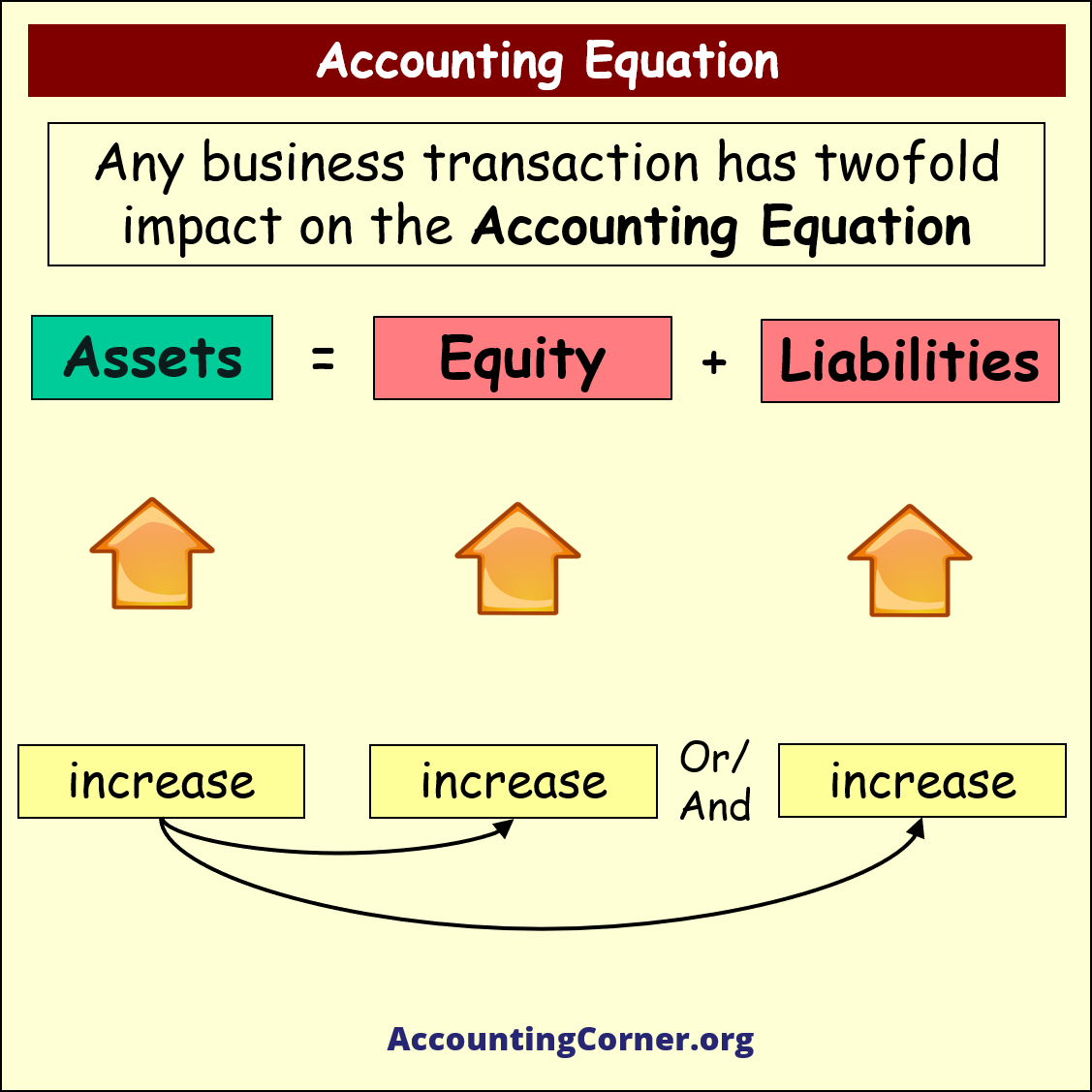

What Is the Accounting Equation?

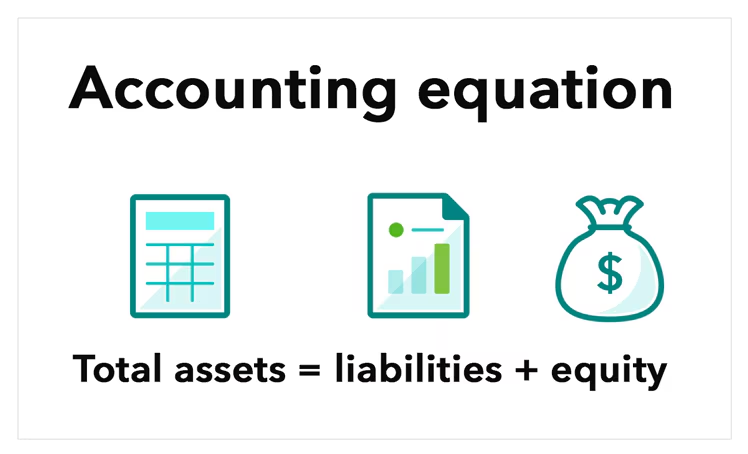

The accounting equation is the foundational formula of double-entry bookkeeping. It states that:

Assets = Liabilities + Equity

The Golden Formula of Accounting

This equation tells us that everything a business owns (assets) has been financed either by borrowing money from someone (liabilities) or by the owner’s own investment (equity). At all times, both sides of this equation must be equal — that’s why it’s called a “balanced” equation. If it ever goes out of balance, it means an error has been made somewhere in the books.

The Basic Accounting Equation — Assets = Liabilities + Equity

Breaking Down Each Component

To truly understand the accounting equation, you need to understand what each of the three components actually means in the real world. Let’s go through each one carefully.

1. Assets — What the Business Owns

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?

This is one of the most common questions beginers ask. The answer lies in the double-entry bookkeeping system. Every single financial transaction affects at least two accounts — one is debited and another is credited — and both sides are always equal. This means no matter how many transactions a business records, the accounting equation will always remain in balance.

Think of it like a seesaw — whenever something is added to one side, something equal is either added to the other side or removed from the same side. The balance is always maintained automaticaly by the nature of double-entry accounting itself.

The Accounting Equation in Action — Real Examples

Let’s walk through some practical transactions to see how the accounting equation stays balanced in every situation. This is where theory meets reality.

How Transactions Affect the Accounting Equation

Example 1 — Owner Invests Cash

Transaction: Sarah starts a business by investing $50,000 of her own cash.

✅ Assets increase: Cash +$50,000

✅ Equity increases: Capital +$50,000

$50,000 = $0 + $50,000 ✔ Balanced

Example 2 — Bought Equipment on Loan

Transaction: Business takes a bank loan of $20,000 to purchase machinery.

✅ Assets increase: Machinery +$20,000

✅ Liabilities increase: Bank Loan +$20,000

$70,000 = $20,000 + $50,000 ✔ Balanced

Example 3 — Earned Revenue

Transaction: Business earns $8,000 by providing services to a client.

✅ Assets increase: Cash +$8,000

✅ Equity increases: Retained Earnings +$8,000

$78,000 = $20,000 + $58,000 ✔ Balanced

Example 4 — Paid an Expense

Transaction: Business pays $2,000 cash as office rent.

✅ Assets decrease: Cash -$2,000

✅ Equity decreases: Retained Earnings -$2,000

$76,000 = $20,000 + $56,000 ✔ Balanced

The Accounting Equation and the Balance Sheet

The balance sheet is basically the accounting equation presented in a formal document. When a business prepares its balance sheet at the end of an accounting period, it is simply organizing all its assets on one side and all its liabilities and equity on the other side — and proving that both sides are equal.

This is why the balance sheet is sometimes called the “Statement of Financial Position” — because it shows the exact financial position of a business at a specific point in time. If your balance sheet balances, it means all your transactions have been recorded corectly. If it doesn’t balance, somthing went wrong and you need to find the error.

Sample Balance Sheet — Assets = Liabilities + Equity

Extended Accounting Equation

As you go deeper into accounting, you’ll come across a more expanded version of the basic equation. Since equity is made up of several components, the equation can be written as:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

Expanded form showing all equity components

This expanded version is extremly useful for understanding how day-to-day business activities like earning revenue, paying expenses, and making withdrawals all affect the overall financial position. Each component plays its own role in either increasing or decreasing the owner’s equity.

Extended Accounting Equation with Revenue, Expenses & Drawings

| Component | Effect on Equity | Example |

|---|---|---|

| Capital Invested | Increases ↑ | Owner puts money in |

| Revenue Earned | Increases ↑ | Sales, service income |

| Expenses Paid | Decreases ↓ | Rent, salaries, utilities |

| Drawings | Decreases ↓ | Owner withdraws cash |

Common Mistakes Beginners Make

Mistake 1 — Thinking Assets Must Always Be Larger: Many beginers assume that a business with more assets is always in better shape. But if those assets are mostly financed through debt (liabilities), the business could actually be in a risky financial position. Always look at the equity portion too.

Mistake 2 — Forgetting That Expenses Reduce Equity: A lot of students forget that when a business pays an expense, it doesn’t just reduce assets — it also reduces equity through retained earnings. Both sides must reflect this change for the equation to stay balanced.

Mistake 3 — Confusing Drawings with Expenses: Owner’s drawings are not business expenses — they are withdrawals from equity. Many small business owners mix these up and end up with inacurate financial statements. Always record drawings as a reduction in equity, not as an operating expense.

Quick Memory Trick 💡

Remember the accounting equation with this simple phrase:

“What you OWN = What you OWE + What’s YOURS”

Liabilities = Owe

Equity = Yours

Always Balanced

Final Thoughts

The accounting equation — Assets = Liabilities + Equity — is not just a formula you memorize for an exam and then forget. It is the living, breathing foundation of every financial transaction your business ever records. Every invoice, every payment, every loan, every sale — all of it flows through this single equation.

Once you really understand what assets, liabilities, and equity mean — and how they interact with each other — reading a balance sheet stops feeling intimidating and starts feeling like reading a story about a business. A story about where the money came from, where it went, and what’s left at the end of the day.

Master this equation, and you’ve mastered the language of accounting.

To truly understand the accounting equation, you need to understand what each of the three components actually means in the real world. Let’s go through each one carefully.

1. Assets — What the Business Owns

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?

This is one of the most common questions beginers ask. The answer lies in the double-entry bookkeeping system. Every single financial transaction affects at least two accounts — one is debited and another is credited — and both sides are always equal. This means no matter how many transactions a business records, the accounting equation will always remain in balance.

Think of it like a seesaw — whenever something is added to one side, something equal is either added to the other side or removed from the same side. The balance is always maintained automaticaly by the nature of double-entry accounting itself.

The Accounting Equation in Action — Real Examples

Let’s walk through some practical transactions to see how the accounting equation stays balanced in every situation. This is where theory meets reality.

How Transactions Affect the Accounting Equation

Example 1 — Owner Invests Cash

Transaction: Sarah starts a business by investing $50,000 of her own cash.

✅ Assets increase: Cash +$50,000

✅ Equity increases: Capital +$50,000

$50,000 = $0 + $50,000 ✔ Balanced

Example 2 — Bought Equipment on Loan

Transaction: Business takes a bank loan of $20,000 to purchase machinery.

✅ Assets increase: Machinery +$20,000

✅ Liabilities increase: Bank Loan +$20,000

$70,000 = $20,000 + $50,000 ✔ Balanced

Example 3 — Earned Revenue

Transaction: Business earns $8,000 by providing services to a client.

✅ Assets increase: Cash +$8,000

✅ Equity increases: Retained Earnings +$8,000

$78,000 = $20,000 + $58,000 ✔ Balanced

Example 4 — Paid an Expense

Transaction: Business pays $2,000 cash as office rent.

✅ Assets decrease: Cash -$2,000

✅ Equity decreases: Retained Earnings -$2,000

$76,000 = $20,000 + $56,000 ✔ Balanced

The Accounting Equation and the Balance Sheet

The balance sheet is basically the accounting equation presented in a formal document. When a business prepares its balance sheet at the end of an accounting period, it is simply organizing all its assets on one side and all its liabilities and equity on the other side — and proving that both sides are equal.

This is why the balance sheet is sometimes called the “Statement of Financial Position” — because it shows the exact financial position of a business at a specific point in time. If your balance sheet balances, it means all your transactions have been recorded corectly. If it doesn’t balance, somthing went wrong and you need to find the error.

Sample Balance Sheet — Assets = Liabilities + Equity

Extended Accounting Equation

As you go deeper into accounting, you’ll come across a more expanded version of the basic equation. Since equity is made up of several components, the equation can be written as:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

Expanded form showing all equity components

This expanded version is extremly useful for understanding how day-to-day business activities like earning revenue, paying expenses, and making withdrawals all affect the overall financial position. Each component plays its own role in either increasing or decreasing the owner’s equity.

Extended Accounting Equation with Revenue, Expenses & Drawings

| Component | Effect on Equity | Example |

|---|---|---|

| Capital Invested | Increases ↑ | Owner puts money in |

| Revenue Earned | Increases ↑ | Sales, service income |

| Expenses Paid | Decreases ↓ | Rent, salaries, utilities |

| Drawings | Decreases ↓ | Owner withdraws cash |

Common Mistakes Beginners Make

Mistake 1 — Thinking Assets Must Always Be Larger: Many beginers assume that a business with more assets is always in better shape. But if those assets are mostly financed through debt (liabilities), the business could actually be in a risky financial position. Always look at the equity portion too.

Mistake 2 — Forgetting That Expenses Reduce Equity: A lot of students forget that when a business pays an expense, it doesn’t just reduce assets — it also reduces equity through retained earnings. Both sides must reflect this change for the equation to stay balanced.

Mistake 3 — Confusing Drawings with Expenses: Owner’s drawings are not business expenses — they are withdrawals from equity. Many small business owners mix these up and end up with inacurate financial statements. Always record drawings as a reduction in equity, not as an operating expense.

Quick Memory Trick 💡

Remember the accounting equation with this simple phrase:

“What you OWN = What you OWE + What’s YOURS”

Liabilities = Owe

Equity = Yours

Always Balanced

Final Thoughts

The accounting equation — Assets = Liabilities + Equity — is not just a formula you memorize for an exam and then forget. It is the living, breathing foundation of every financial transaction your business ever records. Every invoice, every payment, every loan, every sale — all of it flows through this single equation.

Once you really understand what assets, liabilities, and equity mean — and how they interact with each other — reading a balance sheet stops feeling intimidating and starts feeling like reading a story about a business. A story about where the money came from, where it went, and what’s left at the end of the day.

Master this equation, and you’ve mastered the language of accounting.

If there’s one formula that every accountant, student, or business owner absolutly must know — it’s the accounting equation. Three simple words: Assets, Liabilities, and Equity. But behind those three words lies the entire logic of how modern accounting works.

Whether you’re just starting to learn accounting, running a small business, or trying to make sence of a balance sheet for the first time — understanding the accounting equation is the single best place to start. In this article, we’ll break down what the accounting equation actually means, why it always stays balanced, how each component works, and how it connects to real business transactions. By the end, you’ll see why this simple formula is the backbone of all financial reporting.

What Is the Accounting Equation?

The accounting equation is the foundational formula of double-entry bookkeeping. It states that:

Assets = Liabilities + Equity

The Golden Formula of Accounting

This equation tells us that everything a business owns (assets) has been financed either by borrowing money from someone (liabilities) or by the owner’s own investment (equity). At all times, both sides of this equation must be equal — that’s why it’s called a “balanced” equation. If it ever goes out of balance, it means an error has been made somewhere in the books.

The Basic Accounting Equation — Assets = Liabilities + Equity

Breaking Down Each Component

To truly understand the accounting equation, you need to understand what each of the three components actually means in the real world. Let’s go through each one carefully.

1. Assets — What the Business Owns

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?

This is one of the most common questions beginers ask. The answer lies in the double-entry bookkeeping system. Every single financial transaction affects at least two accounts — one is debited and another is credited — and both sides are always equal. This means no matter how many transactions a business records, the accounting equation will always remain in balance.

Think of it like a seesaw — whenever something is added to one side, something equal is either added to the other side or removed from the same side. The balance is always maintained automaticaly by the nature of double-entry accounting itself.

The Accounting Equation in Action — Real Examples

Let’s walk through some practical transactions to see how the accounting equation stays balanced in every situation. This is where theory meets reality.

How Transactions Affect the Accounting Equation

Example 1 — Owner Invests Cash

Transaction: Sarah starts a business by investing $50,000 of her own cash.

✅ Assets increase: Cash +$50,000

✅ Equity increases: Capital +$50,000

$50,000 = $0 + $50,000 ✔ Balanced

Example 2 — Bought Equipment on Loan

Transaction: Business takes a bank loan of $20,000 to purchase machinery.

✅ Assets increase: Machinery +$20,000

✅ Liabilities increase: Bank Loan +$20,000

$70,000 = $20,000 + $50,000 ✔ Balanced

Example 3 — Earned Revenue

Transaction: Business earns $8,000 by providing services to a client.

✅ Assets increase: Cash +$8,000

✅ Equity increases: Retained Earnings +$8,000

$78,000 = $20,000 + $58,000 ✔ Balanced

Example 4 — Paid an Expense

Transaction: Business pays $2,000 cash as office rent.

✅ Assets decrease: Cash -$2,000

✅ Equity decreases: Retained Earnings -$2,000

$76,000 = $20,000 + $56,000 ✔ Balanced

The Accounting Equation and the Balance Sheet

The balance sheet is basically the accounting equation presented in a formal document. When a business prepares its balance sheet at the end of an accounting period, it is simply organizing all its assets on one side and all its liabilities and equity on the other side — and proving that both sides are equal.

This is why the balance sheet is sometimes called the “Statement of Financial Position” — because it shows the exact financial position of a business at a specific point in time. If your balance sheet balances, it means all your transactions have been recorded corectly. If it doesn’t balance, somthing went wrong and you need to find the error.

Sample Balance Sheet — Assets = Liabilities + Equity

Extended Accounting Equation

As you go deeper into accounting, you’ll come across a more expanded version of the basic equation. Since equity is made up of several components, the equation can be written as:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

Expanded form showing all equity components

This expanded version is extremly useful for understanding how day-to-day business activities like earning revenue, paying expenses, and making withdrawals all affect the overall financial position. Each component plays its own role in either increasing or decreasing the owner’s equity.

Extended Accounting Equation with Revenue, Expenses & Drawings

| Component | Effect on Equity | Example |

|---|---|---|

| Capital Invested | Increases ↑ | Owner puts money in |

| Revenue Earned | Increases ↑ | Sales, service income |

| Expenses Paid | Decreases ↓ | Rent, salaries, utilities |

| Drawings | Decreases ↓ | Owner withdraws cash |

Common Mistakes Beginners Make

Mistake 1 — Thinking Assets Must Always Be Larger: Many beginers assume that a business with more assets is always in better shape. But if those assets are mostly financed through debt (liabilities), the business could actually be in a risky financial position. Always look at the equity portion too.

Mistake 2 — Forgetting That Expenses Reduce Equity: A lot of students forget that when a business pays an expense, it doesn’t just reduce assets — it also reduces equity through retained earnings. Both sides must reflect this change for the equation to stay balanced.

Mistake 3 — Confusing Drawings with Expenses: Owner’s drawings are not business expenses — they are withdrawals from equity. Many small business owners mix these up and end up with inacurate financial statements. Always record drawings as a reduction in equity, not as an operating expense.

Quick Memory Trick 💡

Remember the accounting equation with this simple phrase:

“What you OWN = What you OWE + What’s YOURS”

Liabilities = Owe

Equity = Yours

Always Balanced

Final Thoughts

The accounting equation — Assets = Liabilities + Equity — is not just a formula you memorize for an exam and then forget. It is the living, breathing foundation of every financial transaction your business ever records. Every invoice, every payment, every loan, every sale — all of it flows through this single equation.

Once you really understand what assets, liabilities, and equity mean — and how they interact with each other — reading a balance sheet stops feeling intimidating and starts feeling like reading a story about a business. A story about where the money came from, where it went, and what’s left at the end of the day.

Master this equation, and you’ve mastered the language of accounting.

If there’s one formula that every accountant, student, or business owner absolutly must know — it’s the accounting equation. Three simple words: Assets, Liabilities, and Equity. But behind those three words lies the entire logic of how modern accounting works.

Whether you’re just starting to learn accounting, running a small business, or trying to make sence of a balance sheet for the first time — understanding the accounting equation is the single best place to start. In this article, we’ll break down what the accounting equation actually means, why it always stays balanced, how each component works, and how it connects to real business transactions. By the end, you’ll see why this simple formula is the backbone of all financial reporting.

What Is the Accounting Equation?

The accounting equation is the foundational formula of double-entry bookkeeping. It states that:

Assets = Liabilities + Equity

The Golden Formula of Accounting

This equation tells us that everything a business owns (assets) has been financed either by borrowing money from someone (liabilities) or by the owner’s own investment (equity). At all times, both sides of this equation must be equal — that’s why it’s called a “balanced” equation. If it ever goes out of balance, it means an error has been made somewhere in the books.

The Basic Accounting Equation — Assets = Liabilities + Equity

Breaking Down Each Component

To truly understand the accounting equation, you need to understand what each of the three components actually means in the real world. Let’s go through each one carefully.

1. Assets — What the Business Owns

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?

This is one of the most common questions beginers ask. The answer lies in the double-entry bookkeeping system. Every single financial transaction affects at least two accounts — one is debited and another is credited — and both sides are always equal. This means no matter how many transactions a business records, the accounting equation will always remain in balance.

Think of it like a seesaw — whenever something is added to one side, something equal is either added to the other side or removed from the same side. The balance is always maintained automaticaly by the nature of double-entry accounting itself.

The Accounting Equation in Action — Real Examples

Let’s walk through some practical transactions to see how the accounting equation stays balanced in every situation. This is where theory meets reality.

How Transactions Affect the Accounting Equation

Example 1 — Owner Invests Cash

Transaction: Sarah starts a business by investing $50,000 of her own cash.

✅ Assets increase: Cash +$50,000

✅ Equity increases: Capital +$50,000

$50,000 = $0 + $50,000 ✔ Balanced

Example 2 — Bought Equipment on Loan

Transaction: Business takes a bank loan of $20,000 to purchase machinery.

✅ Assets increase: Machinery +$20,000

✅ Liabilities increase: Bank Loan +$20,000

$70,000 = $20,000 + $50,000 ✔ Balanced

Example 3 — Earned Revenue

Transaction: Business earns $8,000 by providing services to a client.

✅ Assets increase: Cash +$8,000

✅ Equity increases: Retained Earnings +$8,000

$78,000 = $20,000 + $58,000 ✔ Balanced

Example 4 — Paid an Expense

Transaction: Business pays $2,000 cash as office rent.

✅ Assets decrease: Cash -$2,000

✅ Equity decreases: Retained Earnings -$2,000

$76,000 = $20,000 + $56,000 ✔ Balanced

The Accounting Equation and the Balance Sheet

The balance sheet is basically the accounting equation presented in a formal document. When a business prepares its balance sheet at the end of an accounting period, it is simply organizing all its assets on one side and all its liabilities and equity on the other side — and proving that both sides are equal.

This is why the balance sheet is sometimes called the “Statement of Financial Position” — because it shows the exact financial position of a business at a specific point in time. If your balance sheet balances, it means all your transactions have been recorded corectly. If it doesn’t balance, somthing went wrong and you need to find the error.

Sample Balance Sheet — Assets = Liabilities + Equity

Extended Accounting Equation

As you go deeper into accounting, you’ll come across a more expanded version of the basic equation. Since equity is made up of several components, the equation can be written as:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

Expanded form showing all equity components

This expanded version is extremly useful for understanding how day-to-day business activities like earning revenue, paying expenses, and making withdrawals all affect the overall financial position. Each component plays its own role in either increasing or decreasing the owner’s equity.

Extended Accounting Equation with Revenue, Expenses & Drawings

| Component | Effect on Equity | Example |

|---|---|---|

| Capital Invested | Increases ↑ | Owner puts money in |

| Revenue Earned | Increases ↑ | Sales, service income |

| Expenses Paid | Decreases ↓ | Rent, salaries, utilities |

| Drawings | Decreases ↓ | Owner withdraws cash |

Common Mistakes Beginners Make

Mistake 1 — Thinking Assets Must Always Be Larger: Many beginers assume that a business with more assets is always in better shape. But if those assets are mostly financed through debt (liabilities), the business could actually be in a risky financial position. Always look at the equity portion too.

Mistake 2 — Forgetting That Expenses Reduce Equity: A lot of students forget that when a business pays an expense, it doesn’t just reduce assets — it also reduces equity through retained earnings. Both sides must reflect this change for the equation to stay balanced.

Mistake 3 — Confusing Drawings with Expenses: Owner’s drawings are not business expenses — they are withdrawals from equity. Many small business owners mix these up and end up with inacurate financial statements. Always record drawings as a reduction in equity, not as an operating expense.

Quick Memory Trick 💡

Remember the accounting equation with this simple phrase:

“What you OWN = What you OWE + What’s YOURS”

Liabilities = Owe

Equity = Yours

Always Balanced

Final Thoughts

The accounting equation — Assets = Liabilities + Equity — is not just a formula you memorize for an exam and then forget. It is the living, breathing foundation of every financial transaction your business ever records. Every invoice, every payment, every loan, every sale — all of it flows through this single equation.

Once you really understand what assets, liabilities, and equity mean — and how they interact with each other — reading a balance sheet stops feeling intimidating and starts feeling like reading a story about a business. A story about where the money came from, where it went, and what’s left at the end of the day.

Master this equation, and you’ve mastered the language of accounting.

To truly understand the accounting equation, you need to understand what each of the three components actually means in the real world. Let’s go through each one carefully.

1. Assets — What the Business Owns

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?

This is one of the most common questions beginers ask. The answer lies in the double-entry bookkeeping system. Every single financial transaction affects at least two accounts — one is debited and another is credited — and both sides are always equal. This means no matter how many transactions a business records, the accounting equation will always remain in balance.

Think of it like a seesaw — whenever something is added to one side, something equal is either added to the other side or removed from the same side. The balance is always maintained automaticaly by the nature of double-entry accounting itself.

The Accounting Equation in Action — Real Examples

Let’s walk through some practical transactions to see how the accounting equation stays balanced in every situation. This is where theory meets reality.

How Transactions Affect the Accounting Equation

Example 1 — Owner Invests Cash

Transaction: Sarah starts a business by investing $50,000 of her own cash.

✅ Assets increase: Cash +$50,000

✅ Equity increases: Capital +$50,000

$50,000 = $0 + $50,000 ✔ Balanced

Example 2 — Bought Equipment on Loan

Transaction: Business takes a bank loan of $20,000 to purchase machinery.

✅ Assets increase: Machinery +$20,000

✅ Liabilities increase: Bank Loan +$20,000

$70,000 = $20,000 + $50,000 ✔ Balanced

Example 3 — Earned Revenue

Transaction: Business earns $8,000 by providing services to a client.

✅ Assets increase: Cash +$8,000

✅ Equity increases: Retained Earnings +$8,000

$78,000 = $20,000 + $58,000 ✔ Balanced

Example 4 — Paid an Expense

Transaction: Business pays $2,000 cash as office rent.

✅ Assets decrease: Cash -$2,000

✅ Equity decreases: Retained Earnings -$2,000

$76,000 = $20,000 + $56,000 ✔ Balanced

The Accounting Equation and the Balance Sheet

The balance sheet is basically the accounting equation presented in a formal document. When a business prepares its balance sheet at the end of an accounting period, it is simply organizing all its assets on one side and all its liabilities and equity on the other side — and proving that both sides are equal.

This is why the balance sheet is sometimes called the “Statement of Financial Position” — because it shows the exact financial position of a business at a specific point in time. If your balance sheet balances, it means all your transactions have been recorded corectly. If it doesn’t balance, somthing went wrong and you need to find the error.

Sample Balance Sheet — Assets = Liabilities + Equity

Extended Accounting Equation

As you go deeper into accounting, you’ll come across a more expanded version of the basic equation. Since equity is made up of several components, the equation can be written as:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

Expanded form showing all equity components

This expanded version is extremly useful for understanding how day-to-day business activities like earning revenue, paying expenses, and making withdrawals all affect the overall financial position. Each component plays its own role in either increasing or decreasing the owner’s equity.

Extended Accounting Equation with Revenue, Expenses & Drawings

| Component | Effect on Equity | Example |

|---|---|---|

| Capital Invested | Increases ↑ | Owner puts money in |

| Revenue Earned | Increases ↑ | Sales, service income |

| Expenses Paid | Decreases ↓ | Rent, salaries, utilities |

| Drawings | Decreases ↓ | Owner withdraws cash |

Common Mistakes Beginners Make

Mistake 1 — Thinking Assets Must Always Be Larger: Many beginers assume that a business with more assets is always in better shape. But if those assets are mostly financed through debt (liabilities), the business could actually be in a risky financial position. Always look at the equity portion too.

Mistake 2 — Forgetting That Expenses Reduce Equity: A lot of students forget that when a business pays an expense, it doesn’t just reduce assets — it also reduces equity through retained earnings. Both sides must reflect this change for the equation to stay balanced.

Mistake 3 — Confusing Drawings with Expenses: Owner’s drawings are not business expenses — they are withdrawals from equity. Many small business owners mix these up and end up with inacurate financial statements. Always record drawings as a reduction in equity, not as an operating expense.

Quick Memory Trick 💡

Remember the accounting equation with this simple phrase:

“What you OWN = What you OWE + What’s YOURS”

Liabilities = Owe

Equity = Yours

Always Balanced

Final Thoughts

The accounting equation — Assets = Liabilities + Equity — is not just a formula you memorize for an exam and then forget. It is the living, breathing foundation of every financial transaction your business ever records. Every invoice, every payment, every loan, every sale — all of it flows through this single equation.

Once you really understand what assets, liabilities, and equity mean — and how they interact with each other — reading a balance sheet stops feeling intimidating and starts feeling like reading a story about a business. A story about where the money came from, where it went, and what’s left at the end of the day.

Master this equation, and you’ve mastered the language of accounting.

If there’s one formula that every accountant, student, or business owner absolutly must know — it’s the accounting equation. Three simple words: Assets, Liabilities, and Equity. But behind those three words lies the entire logic of how modern accounting works.

Whether you’re just starting to learn accounting, running a small business, or trying to make sence of a balance sheet for the first time — understanding the accounting equation is the single best place to start. In this article, we’ll break down what the accounting equation actually means, why it always stays balanced, how each component works, and how it connects to real business transactions. By the end, you’ll see why this simple formula is the backbone of all financial reporting.

What Is the Accounting Equation?

The accounting equation is the foundational formula of double-entry bookkeeping. It states that:

Assets = Liabilities + Equity

The Golden Formula of Accounting

This equation tells us that everything a business owns (assets) has been financed either by borrowing money from someone (liabilities) or by the owner’s own investment (equity). At all times, both sides of this equation must be equal — that’s why it’s called a “balanced” equation. If it ever goes out of balance, it means an error has been made somewhere in the books.

The Basic Accounting Equation — Assets = Liabilities + Equity

Breaking Down Each Component

To truly understand the accounting equation, you need to understand what each of the three components actually means in the real world. Let’s go through each one carefully.

1. Assets — What the Business Owns

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?

This is one of the most common questions beginers ask. The answer lies in the double-entry bookkeeping system. Every single financial transaction affects at least two accounts — one is debited and another is credited — and both sides are always equal. This means no matter how many transactions a business records, the accounting equation will always remain in balance.

Think of it like a seesaw — whenever something is added to one side, something equal is either added to the other side or removed from the same side. The balance is always maintained automaticaly by the nature of double-entry accounting itself.

The Accounting Equation in Action — Real Examples

Let’s walk through some practical transactions to see how the accounting equation stays balanced in every situation. This is where theory meets reality.

How Transactions Affect the Accounting Equation

Example 1 — Owner Invests Cash

Transaction: Sarah starts a business by investing $50,000 of her own cash.

✅ Assets increase: Cash +$50,000

✅ Equity increases: Capital +$50,000

$50,000 = $0 + $50,000 ✔ Balanced

Example 2 — Bought Equipment on Loan

Transaction: Business takes a bank loan of $20,000 to purchase machinery.

✅ Assets increase: Machinery +$20,000

✅ Liabilities increase: Bank Loan +$20,000

$70,000 = $20,000 + $50,000 ✔ Balanced

Example 3 — Earned Revenue

Transaction: Business earns $8,000 by providing services to a client.

✅ Assets increase: Cash +$8,000

✅ Equity increases: Retained Earnings +$8,000

$78,000 = $20,000 + $58,000 ✔ Balanced

Example 4 — Paid an Expense

Transaction: Business pays $2,000 cash as office rent.

✅ Assets decrease: Cash -$2,000

✅ Equity decreases: Retained Earnings -$2,000

$76,000 = $20,000 + $56,000 ✔ Balanced

The Accounting Equation and the Balance Sheet

The balance sheet is basically the accounting equation presented in a formal document. When a business prepares its balance sheet at the end of an accounting period, it is simply organizing all its assets on one side and all its liabilities and equity on the other side — and proving that both sides are equal.

This is why the balance sheet is sometimes called the “Statement of Financial Position” — because it shows the exact financial position of a business at a specific point in time. If your balance sheet balances, it means all your transactions have been recorded corectly. If it doesn’t balance, somthing went wrong and you need to find the error.

Sample Balance Sheet — Assets = Liabilities + Equity

Extended Accounting Equation

As you go deeper into accounting, you’ll come across a more expanded version of the basic equation. Since equity is made up of several components, the equation can be written as:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

Expanded form showing all equity components

This expanded version is extremly useful for understanding how day-to-day business activities like earning revenue, paying expenses, and making withdrawals all affect the overall financial position. Each component plays its own role in either increasing or decreasing the owner’s equity.

Extended Accounting Equation with Revenue, Expenses & Drawings

| Component | Effect on Equity | Example |

|---|---|---|

| Capital Invested | Increases ↑ | Owner puts money in |

| Revenue Earned | Increases ↑ | Sales, service income |

| Expenses Paid | Decreases ↓ | Rent, salaries, utilities |

| Drawings | Decreases ↓ | Owner withdraws cash |

Common Mistakes Beginners Make

Mistake 1 — Thinking Assets Must Always Be Larger: Many beginers assume that a business with more assets is always in better shape. But if those assets are mostly financed through debt (liabilities), the business could actually be in a risky financial position. Always look at the equity portion too.

Mistake 2 — Forgetting That Expenses Reduce Equity: A lot of students forget that when a business pays an expense, it doesn’t just reduce assets — it also reduces equity through retained earnings. Both sides must reflect this change for the equation to stay balanced.

Mistake 3 — Confusing Drawings with Expenses: Owner’s drawings are not business expenses — they are withdrawals from equity. Many small business owners mix these up and end up with inacurate financial statements. Always record drawings as a reduction in equity, not as an operating expense.

Quick Memory Trick 💡

Remember the accounting equation with this simple phrase:

“What you OWN = What you OWE + What’s YOURS”

Liabilities = Owe

Equity = Yours

Always Balanced

Final Thoughts

The accounting equation — Assets = Liabilities + Equity — is not just a formula you memorize for an exam and then forget. It is the living, breathing foundation of every financial transaction your business ever records. Every invoice, every payment, every loan, every sale — all of it flows through this single equation.

Once you really understand what assets, liabilities, and equity mean — and how they interact with each other — reading a balance sheet stops feeling intimidating and starts feeling like reading a story about a business. A story about where the money came from, where it went, and what’s left at the end of the day.

Master this equation, and you’ve mastered the language of accounting.

To truly understand the accounting equation, you need to understand what each of the three components actually means in the real world. Let’s go through each one carefully.

1. Assets — What the Business Owns

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?

This is one of the most common questions beginers ask. The answer lies in the double-entry bookkeeping system. Every single financial transaction affects at least two accounts — one is debited and another is credited — and both sides are always equal. This means no matter how many transactions a business records, the accounting equation will always remain in balance.

Think of it like a seesaw — whenever something is added to one side, something equal is either added to the other side or removed from the same side. The balance is always maintained automaticaly by the nature of double-entry accounting itself.

The Accounting Equation in Action — Real Examples

Let’s walk through some practical transactions to see how the accounting equation stays balanced in every situation. This is where theory meets reality.

How Transactions Affect the Accounting Equation

Example 1 — Owner Invests Cash

Transaction: Sarah starts a business by investing $50,000 of her own cash.

✅ Assets increase: Cash +$50,000

✅ Equity increases: Capital +$50,000

$50,000 = $0 + $50,000 ✔ Balanced

Example 2 — Bought Equipment on Loan

Transaction: Business takes a bank loan of $20,000 to purchase machinery.

✅ Assets increase: Machinery +$20,000

✅ Liabilities increase: Bank Loan +$20,000

$70,000 = $20,000 + $50,000 ✔ Balanced

Example 3 — Earned Revenue

Transaction: Business earns $8,000 by providing services to a client.

✅ Assets increase: Cash +$8,000

✅ Equity increases: Retained Earnings +$8,000

$78,000 = $20,000 + $58,000 ✔ Balanced

Example 4 — Paid an Expense

Transaction: Business pays $2,000 cash as office rent.

✅ Assets decrease: Cash -$2,000

✅ Equity decreases: Retained Earnings -$2,000

$76,000 = $20,000 + $56,000 ✔ Balanced

The Accounting Equation and the Balance Sheet

The balance sheet is basically the accounting equation presented in a formal document. When a business prepares its balance sheet at the end of an accounting period, it is simply organizing all its assets on one side and all its liabilities and equity on the other side — and proving that both sides are equal.

This is why the balance sheet is sometimes called the “Statement of Financial Position” — because it shows the exact financial position of a business at a specific point in time. If your balance sheet balances, it means all your transactions have been recorded corectly. If it doesn’t balance, somthing went wrong and you need to find the error.

Sample Balance Sheet — Assets = Liabilities + Equity

Extended Accounting Equation

As you go deeper into accounting, you’ll come across a more expanded version of the basic equation. Since equity is made up of several components, the equation can be written as:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

Expanded form showing all equity components

This expanded version is extremly useful for understanding how day-to-day business activities like earning revenue, paying expenses, and making withdrawals all affect the overall financial position. Each component plays its own role in either increasing or decreasing the owner’s equity.

Extended Accounting Equation with Revenue, Expenses & Drawings

| Component | Effect on Equity | Example |

|---|---|---|

| Capital Invested | Increases ↑ | Owner puts money in |

| Revenue Earned | Increases ↑ | Sales, service income |

| Expenses Paid | Decreases ↓ | Rent, salaries, utilities |

| Drawings | Decreases ↓ | Owner withdraws cash |

Common Mistakes Beginners Make

Mistake 1 — Thinking Assets Must Always Be Larger: Many beginers assume that a business with more assets is always in better shape. But if those assets are mostly financed through debt (liabilities), the business could actually be in a risky financial position. Always look at the equity portion too.

Mistake 2 — Forgetting That Expenses Reduce Equity: A lot of students forget that when a business pays an expense, it doesn’t just reduce assets — it also reduces equity through retained earnings. Both sides must reflect this change for the equation to stay balanced.

Mistake 3 — Confusing Drawings with Expenses: Owner’s drawings are not business expenses — they are withdrawals from equity. Many small business owners mix these up and end up with inacurate financial statements. Always record drawings as a reduction in equity, not as an operating expense.

Quick Memory Trick 💡

Remember the accounting equation with this simple phrase:

“What you OWN = What you OWE + What’s YOURS”

Liabilities = Owe

Equity = Yours

Always Balanced

Final Thoughts

The accounting equation — Assets = Liabilities + Equity — is not just a formula you memorize for an exam and then forget. It is the living, breathing foundation of every financial transaction your business ever records. Every invoice, every payment, every loan, every sale — all of it flows through this single equation.

Once you really understand what assets, liabilities, and equity mean — and how they interact with each other — reading a balance sheet stops feeling intimidating and starts feeling like reading a story about a business. A story about where the money came from, where it went, and what’s left at the end of the day.

Master this equation, and you’ve mastered the language of accounting.

If there’s one formula that every accountant, student, or business owner absolutly must know — it’s the accounting equation. Three simple words: Assets, Liabilities, and Equity. But behind those three words lies the entire logic of how modern accounting works.

Whether you’re just starting to learn accounting, running a small business, or trying to make sence of a balance sheet for the first time — understanding the accounting equation is the single best place to start. In this article, we’ll break down what the accounting equation actually means, why it always stays balanced, how each component works, and how it connects to real business transactions. By the end, you’ll see why this simple formula is the backbone of all financial reporting.

What Is the Accounting Equation?

The accounting equation is the foundational formula of double-entry bookkeeping. It states that:

Assets = Liabilities + Equity

The Golden Formula of Accounting

This equation tells us that everything a business owns (assets) has been financed either by borrowing money from someone (liabilities) or by the owner’s own investment (equity). At all times, both sides of this equation must be equal — that’s why it’s called a “balanced” equation. If it ever goes out of balance, it means an error has been made somewhere in the books.

The Basic Accounting Equation — Assets = Liabilities + Equity

Breaking Down Each Component

To truly understand the accounting equation, you need to understand what each of the three components actually means in the real world. Let’s go through each one carefully.

1. Assets — What the Business Owns

Assets are everything that a business owns or controls which has economic value. These are the resources a company uses to operate and grow. Assets can be tangible — like cash, equipment, and inventory — or intangible, like patents, trademarks, or goodwill.

Assets are further divided into Current Assets (things that can be converted to cash within one year — like cash, accounts receivable, and stock) and Non-Current Assets (long-term resources like land, buildings, and machinery).

Examples: Cash, Bank Balance, Accounts Receivable, Inventory, Land, Buildings, Machinery, Vehicles, Goodwill, Patents

Current Assets vs Non-Current Assets

2. Liabilities — What the Business Owes

Liabilities are the obligations or debts that a business owes to outsiders. These are claims that creditors, suppliers, banks, or lenders have against the company’s assets. Whenever a business borrows money or purchases something on credit, it creates a liability.

Like assets, liabilities are also divided into Current Liabilities (debts due within one year — like accounts payable and short-term loans) and Non-Current Liabilities (long-term obligations like bank loans and mortgages).

Examples: Accounts Payable, Bank Loans, Mortgages, Salaries Payable, Tax Payable, Outstanding Expensess

3. Equity — What Belongs to the Owner

Equity, also called owner’s equity or shareholder’s equity, represents the owner’s residual interest in the business after all liabilities have been subtracted from assets. In simple words, it’s what the owner would be left with if the business sold everything it owned and paid off all its debts.

Equity increases when the owner invests more money into the business or when the business earns profits. It decreases when the owner withdraws money (drawings) or when the business incurrs losses.

Examples: Owner’s Capital, Retained Earnings, Share Capital, Reserves, Drawings (reduces equity)

Owner’s Equity — What Belongs to the Business Owner

Why Does the Accounting Equation Always Balance?